Daily Bank Reconciliation: The Complete Guide to Accurate Financial Records

What Is Bank Reconciliation — and Why Does It Matter Daily?

Bank reconciliation is the process of comparing your internal financial records against your bank statement to ensure they match. When discrepancies exist, you investigate and resolve them before they compound into bigger problems.

While many businesses reconcile monthly, daily reconciliation offers a powerful advantage: you catch errors, fraud, and cash flow surprises within 24 hours instead of 30 days. For high-volume businesses, this is not optional — it is essential.

The Core Components of a Bank Reconciliation

Every reconciliation compares two sets of records. Understanding what each contains is the foundation of the entire process.

Your Internal Cash Book

This is your company’s own record of all cash transactions — every deposit, payment, transfer, and fee your accounting team has logged. It may live in your accounting system, a spreadsheet, or a general ledger.

Your Bank Statement

This is the official record held by your financial institution. It shows every transaction that has cleared your account, including charges, credits, and holds applied by the bank itself.

The Reconciling Items

Reconciling items are the legitimate differences between the two records at any given moment. Common examples include:

- Outstanding checks — issued by you, not yet cleared at the bank

- Deposits in transit — recorded by you, not yet posted by the bank

- Bank fees or interest — posted by the bank, not yet entered in your books

- Returned checks (NSF) — bounced checks that reduce your bank balance

- Timing differences — transactions recorded on different business days

Step-by-Step: The Daily Bank Reconciliation Process

Gather Your Source Documents

Before you begin, collect everything you need: today’s bank statement or online banking feed, your cash book or accounting system ledger for the same period, prior day’s ending reconciled balance, and any pending transaction notes.

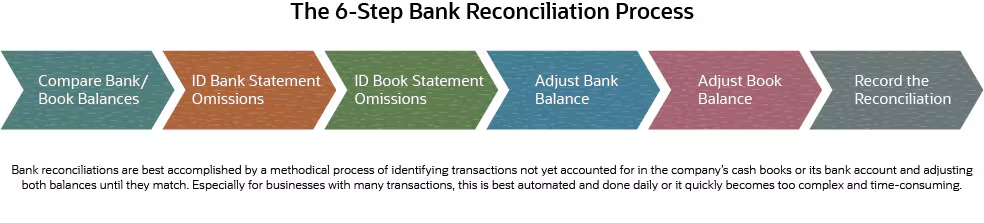

Match Deposits

Go through each deposit in your cash book and confirm it appears on the bank statement. Mark matched items on both sides. Note any deposits you recorded that the bank has not yet processed — these are your deposits in transit.

Match Payments and Withdrawals

Do the same for outgoing transactions. Every check, ACH payment, wire transfer, and debit card charge should match between the two records. Unmatched items on the bank side may be fees or unauthorized charges. Unmatched items on your side are outstanding checks.

Account for Bank-Only Items

Banks apply charges and credits you may not have recorded yet — service fees, interest earned, wire fees, returned items. Enter these into your cash book now so your records stay current.

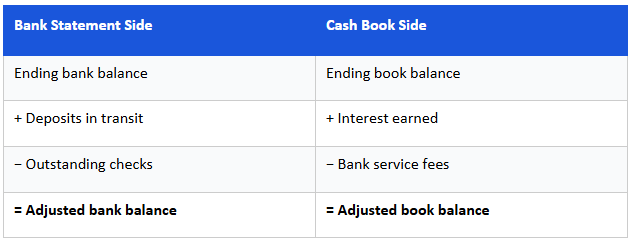

Calculate the Adjusted Balances

Apply the following formula to bring both sides into alignment:

When the adjusted bank balance equals the adjusted book balance, your reconciliation is complete.

Investigate and Resolve Discrepancies

A difference between your adjusted balances means something was missed, misrecorded, or is unauthorized. Common causes include:

- Transposition errors — digits entered in the wrong order

- Duplicate entries — same transaction recorded twice in one system

- Missing transactions — a payment or deposit not yet recorded on one side

- Unauthorized charges — fees or debits you did not authorize

- Returned items — checks or ACH payments that failed and reversed

Document and Sign Off

Once balanced, document the completed reconciliation with the date, preparer name, final adjusted balances, and a list of any reconciling items. A second team member should review and sign off wherever possible — this is a critical internal control.

Common Mistakes That Derail Reconciliations

Even experienced teams make these errors. Awareness is the first line of defense.

- Reconciling to the wrong period — always match statement dates precisely

- Ignoring small discrepancies — even a difference can signal a larger pattern

- Skipping bank-side adjustments — fees and interest must be entered in your books

- Using unreconciled prior balances — always start from a confirmed closing balance

- Rushing the match — visual matching without verification leads to false positives

Internal Controls That Make Daily Reconciliation Stronger

Reconciliation is most powerful when embedded in a system of controls. Consider implementing the following alongside your daily process:

- Segregation of duties — the person who records transactions should not be the one reconciling them

- Dual authorization — require two approvals for transactions above a set threshold

- Exception reporting — flag any transaction above a defined amount for same-day review

- Read-only bank access for reconcilers — prevents accidental or fraudulent modifications

- Locked periods in your accounting system — prevent retroactive changes to reconciled periods

How to Handle High Transaction Volumes

For businesses processing hundreds or thousands of transactions per day, a manual line-by-line approach is not practical. Structure your process to scale:

- Batch matching — group transactions by type (payroll, vendor payments, customer receipts) and reconcile by batch total first

- Automated feeds — connect your bank directly to your accounting system via bank feeds to auto-import and pre-match transactions

- Exception-based review — only manually review unmatched items, not the entire transaction list

- Tolerable difference thresholds — for very high volumes, set a materiality threshold below which auto-cleared items do not require manual review, pending end-of-week full review

Reconciliation for Multiple Accounts

If your business maintains multiple bank accounts — operating, payroll, petty cash, savings — each requires its own reconciliation. Keep them separate and use a master summary to view total cash position across all accounts.

Prioritize accounts in this order: operating accounts first (highest volume, highest risk), then payroll accounts (tight timing requirements), then savings and reserve accounts (lower frequency is acceptable).

Signs Your Reconciliation Process Needs Improvement

Watch for these warning signs in your current process:

- Reconciliation regularly takes more than 30 minutes for a single account

- You frequently carry reconciling items older than 5 business days

- Team members skip the process when busy or understaffed

- Discrepancies are often written off without root cause investigation

- No one reviews completed reconciliations before sign-off

If two or more of these apply, a process review is overdue.

Conclusion

Bank reconciliation is not a back-office chore — it is one of the clearest windows into the financial health of your business. Done daily, it gives you real-time awareness of your cash position, early warning on fraud or errors, and the confidence that your financial records are always audit-ready.

The businesses that treat reconciliation as a daily discipline, rather than a monthly obligation, are the ones that rarely face surprises at month-end, year-end, or tax time.